Posted on March 20, 2024

By Matija Jankovic at MHP’s Center for Housing Data

Massachusetts continues to rank among the most expensive states for renters. With the sluggish pace of housing production relative to the persistently high demand for rental housing, housing affordability is a struggle for many residents of the Commonwealth. Relaxing zoning laws and encouraging more multifamily development are certainly important antidotes but more permissive zoning won’t overcome an intractable and growing issue: the development of new housing has become incredibly expensive, and these high development costs are passed along to renters.

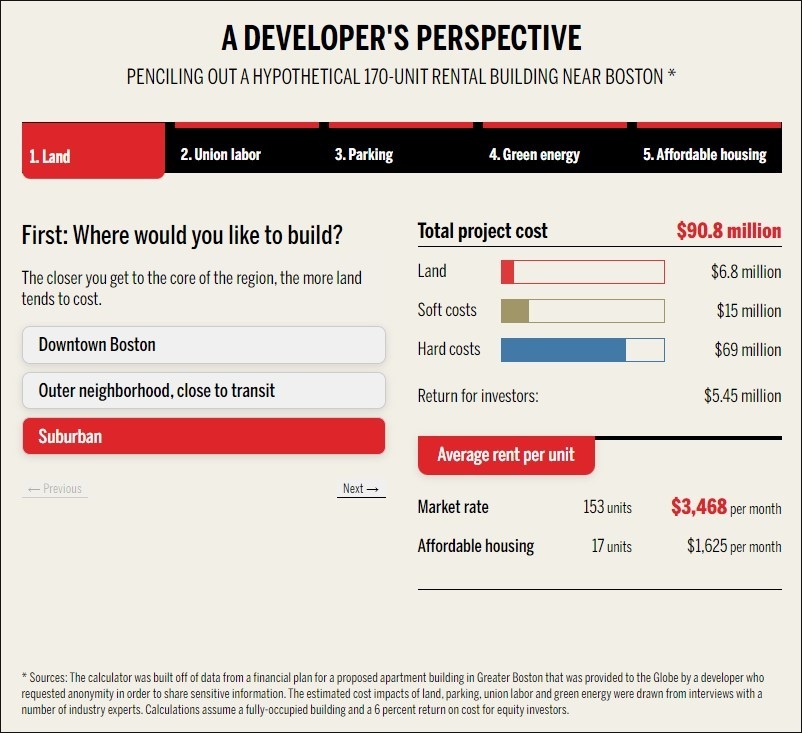

A new report from the Spotlight Team at the Boston Globe reveals that rising construction costs along with complex requirements for building have significantly impacted the economic feasibility of new housing developments. Navigating increasing land, material, and labor costs, alongside a complex terrain of zoning regulations, special permitting processes, and inflated interest rates on construction loans, developers are constrained to building new housing units at high price points to recoup escalating costs while turning a reasonable profit. As noted in the Spotlight report, the hard costs of development—labor and materials—make up roughly 75 to 80 percent of the cost of a new development. To illustrate how these development costs lead to high asking rents, the report features a data tool that estimates monthly rents for a hypothetical 170-unit development in or near Boston based on a variety of inputs: location, labor (union or non-union), abundance of parking, energy efficiency, and integration of affordable units.

The estimates generated by this tool prompted our research team to explore how new construction rents stack up against the incomes of everyday renters in Massachusetts. These estimates are by no means perfect and do not represent potential rents of new developments in their entirety, but they give us a useful frame of reference for exploring affordability trends. Using the Globe’s rent calculator and the five inputs explored in the piece, we generated three price points based on a range of development practices.

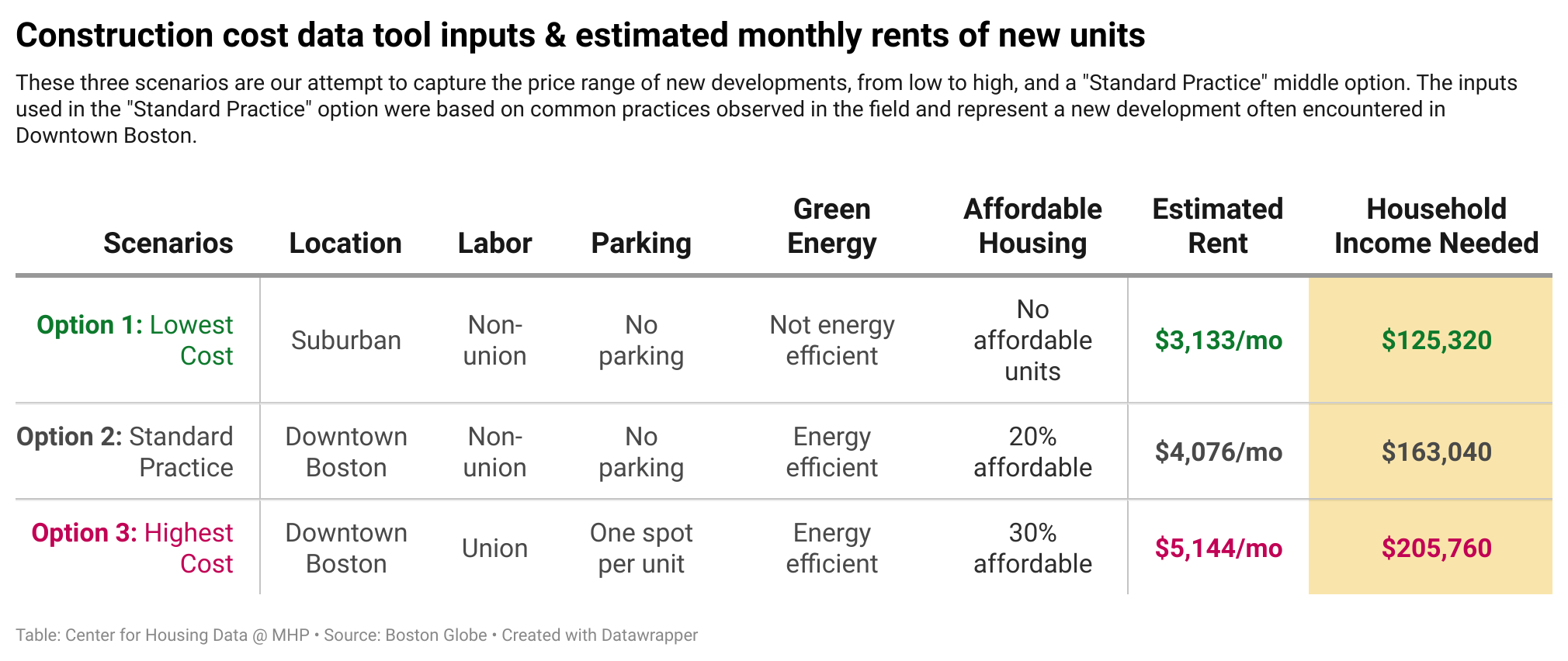

Our three scenarios aim to capture a range of price points for new developments, from the lowest rent based on the inputs provided ($3,133/month), to the highest rent ($5,144/month). The inputs used in our “Standard Practice” option were based on common practices observed in the field and represent a type of new development we often encounter in our downtowns. We included a “Household Income Needed” field in our analysis derived from the estimated rents using the 30-percent rule; at the incomes listed in the table, households would spend no more than 30 of their income on housing costs.

The table above reveals that household incomes needed to afford these new units are quite high, even at the lowest price point. For the middle-of-the-road “Standard Practice” option (a development hypothetically located in Downtown Boston), the household income needed to afford the estimated $4,076/month rent for one of these units is nearly $60,000 higher than the median income in Greater Boston (about $163,000 in needed income relative to a median income of about $104,000). Seeing how these high estimated rents stack up against the region’s median income led us to dig deeper and analyze just how many renters across Massachusetts could afford asking rents at a newly built market-rate housing development.

Expectedly, the findings show that these rents are affordable to a small subset of renter households in Massachusetts. The statewide median household income for renters is roughly $55,900 per year, meaning that around half of all renter households are unable to comfortably afford rents over $1,398 per month. For new construction units, only 19.3 percent of Massachusetts renter households can afford the least expensive market rent; 11.5 percent can afford the middle-of-the-road “Standard Practice” option, and only 6.7 percent can afford the most expensive market rent.

We should all be concerned that so many of our fellow residents are facing affordability challenges given these high prices. A lack of affordability this pervasive reaches households across the state and means that most professions in Massachusetts fail to provide enough income to afford to live here.

According to statewide wage data from the U.S. Bureau of Labor Statistics, average salaries of workers across nearly all occupational groups in Massachusetts fall short of the income needed to afford new construction rents. Legal and management occupations stand out as the two occupation groups with average salaries high enough to afford our lowest cost option ($3,133/mo) but are still insufficient to comfortably afford the estimated “Standard Practice” rent ($4,076/mo). Workers in all other occupational groups did not have average salaries high enough to afford even the lowest cost option.

While this data represents incomes of individual workers rather than households—where multiple incomes may be used toward rent—this suggests that despite relatively high wages for some occupations, most jobs in our state are not paying workers enough to afford the rents of new construction. In many cases, even households with two or more paid workers or households where workers hold multiple jobs would struggle to afford rent in newly constructed apartments.

This presents an issue both for renters searching for homes they can afford and developers looking for a market where development is feasible. With our constrained housing supply, renters across a wide range of incomes will continue to compete for the same units as their monthly rents rise. And without a market that can accommodate the cost of new construction, developers are constrained between building units at high price points or electing to avoid developing housing in Massachusetts altogether. In the long term, new units priced to only accommodate the highest-income households will alter the composition of our population over time, especially relative to socioeconomic diversity. If most new units are unaffordable to most existing renters in Massachusetts, then we are accommodating high-income households while making it increasingly difficult for low-paid workers to make a life here.

We need abundant amounts of new housing, and we need to pursue a level of production that tempers rent levels. However, we are quite far behind in overcoming supply and demand pressures in a way that might achieve that. Census data show that rental vacancy rates in Massachusetts are among the lowest in the last decade. Since 2022, rental vacancy rates have been at or below 3 percent; for reference, a generally accepted vacancy level for a healthy rental housing market is roughly 6 to 8 percent.

Most rental units are filled and competition for housing is high, which has a major role in inflating the already expensive rents impacting households across the state. New research from the Harvard Joint Center for Housing Studies shows rents across the nation are stabilizing due to a major influx of new housing supply as nationwide rental vacancy rates approach 6 percent. While increasing the supply of new housing does not guarantee greater affordability, it is a crucial piece of the puzzle for alleviating the cost burden for renters in high-demand housing markets.

Massachusetts is making coordinated efforts to encourage more multifamily housing development. The new multifamily zoning guidelines for MBTA communities are a major step towards relaxing zoning measures and reducing the often lengthy, expensive, and cumbersome approval process for multifamily development. However, without addressing the inflated costs of housing development and other costly requirements including parking minimums, we may not see the level of development needed to make a significant impact on housing access and affordability.

Reducing construction costs is crucial to ensuring greater affordability for renters in Massachusetts. Based on our exploratory analysis, a 20 percent reduction in construction costs could lead to nearly 8 percent more households—roughly 79,000 households—being able to afford rents in new developments. Strategic interventions such as subsidizing union labor costs for housing development, short-term tax breaks for housing developers, lifting parking minimums and finding creative parking share solutions, or introducing novel construction methods such as modular, factory-built housing units, could aid in creating more rental opportunities for moderate-income renter households while removing barriers for developers.

Addressing housing affordability requires a multifaceted approach to undo unnecessary obstacles to housing production. While boosting housing production, relaxing zoning, and increasing funding for subsidized housing have been well-covered by researchers and the press and have often been incorporated into public policy, less attention has been paid to the role that development costs play in stifling development and increasing rents. Taking proactive steps to address these ballooning costs while continuing to support zoning and subsidy changes is a critical addition to the set of strategies needed to increase the supply of available housing units and reduce the financial burdens faced by renters.

For additional information about this brief or upcoming topics, contact Matija Jankovic.

For more information contact MHP Communication Manager Lisa Braxton, (857) 301-1526.